Connecticut HOA Reserve Studies: Your Non-Negotiable Guide to CIOA Compliance and Financial Health

Find state-specific reserve study requirements and funding laws — choose your state to see what is legally required for reserve studies, updates, and funding levels.

Are you a Connecticut HOA or Condo Board Member, Property Manager, or Reserve Specialist navigating the waters of the Connecticut Common Interest Ownership Act (CIOA)?

Unlike some states with strict, mandatory reserve funding laws, Connecticut offers a nuanced legal landscape. While the state statute doesn't explicitly mandate a reserve study by name, it imposes a critical requirement that effectively makes a professional assessment non-negotiable for responsible governance.

Is a Reserve Study Required or Recommended in Connecticut?

The shortest answer is: It is not legally required, but it is fiduciarily and practically necessary.

The Connecticut General Statutes (CGS), specifically CIOA, do not currently mandate that associations commission a professional, third-party reserve study.1 There are also no state-imposed minimum reserve funding levels.2

However, the legal framework creates a powerful, implied obligation through its disclosure rules.

The CIOA Disclosure Mandate: Your Core Duty

The central legal requirement governing reserves in Connecticut is found in CGS § 47-261e.

This statute requires the executive board to provide unit owners with the proposed annual budget, including:

- A clear statement of the amount held in reserve accounts.

- A statement of the basis on which such reserves are calculated and funded.3

If your board attempts to provide an arbitrary number or a figure pulled from thin air, you are failing the statutory requirement to provide a documented, defensible “basis.” Only a professional reserve study, which analyzes component wear, useful life, and replacement costs, provides the objective financial justification needed to meet this legal duty and defend the board against claims of fiduciary neglect.

The Real Risk: Fannie Mae and Freddie Mac Eligibility

For most Connecticut communities, the threat of legal liability from the state is secondary to the far more devastating risk of losing conventional mortgage eligibility.

Lender guidelines override state law when it comes to the sale of individual units. If your community is non-compliant with these standards, buyers may be unable to secure conventional loans, instantly restricting your market and causing property values to drop.

A professional reserve study is essential to satisfy these entities:

- Replacing the 10% Rule: Lenders (Fannie Mae and Freddie Mac) typically require associations to fund reserves equal to at least 10% of their annual gross budget. However, they will accept a professional reserve study in lieu of the 10% rule if the study demonstrates the project has adequate funded reserves that meet or exceed its own recommendations.4

- Content Requirements: The study must address all major common components, their condition and remaining useful life (RUL), and a suggested funding plan. Crucially, the study must comment favorably on the project's age, structural integrity, and the replacement schedules of major components.5

The Bottom Line: Your reserve study is not just a financial document; it is a project eligibility document that protects the marketability of every unit in your community.

Cadence, Methodology, and Professional Standards

Since Connecticut law is silent on the how and how often, you must follow industry best practices to meet the "basis" disclosure and lending standards.

1. Frequency and Cadence

To remain compliant and financially sound, follow this cycle:

- Full Onsite Study (Level III): Commission a comprehensive, physical, visual inspection by a professional at least once every three to five years.4 This establishes the baseline component data, condition, and remaining useful life.

- Annual Financial Update (Level IV): In the years between full studies, the board must perform an update to adjust component replacement costs for inflation and verify the timing of expenditures. This annual review is crucial for providing an accurate "basis" in every annual budget disclosure.3

2. Who Can Perform the Study?

Connecticut statutes do not require reserve specialists to be licensed or certified by the state.1

However, the executive board is held to a fiduciary duty of prudence. To mitigate personal liability and ensure the report is credible to lenders and owners, boards should only contract with professionals who hold nationally recognized certifications, such as the Community Associations Institute’s (CAI) Reserve Specialist (RS) designation. Using a certified, independent third party is the most reliable way to demonstrate due diligence.

Looking Ahead: The Future of CT Reserve Law

The legislative landscape in Connecticut shows a clear, active intent to move beyond simple disclosure toward mandatory assessments.

In 2025, for example, Senate Bill 816 (SB00816) was introduced with the purpose of requiring the executive board of any common interest community to perform an annual study of the association's reserve funds and make specific recommendations for allocation.6

Although SB00816 was listed as "Dead" in June 2025 6, its introduction is a powerful indicator. HOAs and COAs should anticipate that similar, stricter legislation—potentially requiring mandatory professional studies and minimum funding—will likely be reintroduced and eventually passed in a coming session.

The Strategic Recommendation: Practice strategic over-compliance now. Boards that adopt and adhere to a professional reserve schedule today will be perfectly positioned when the inevitable mandate arrives.

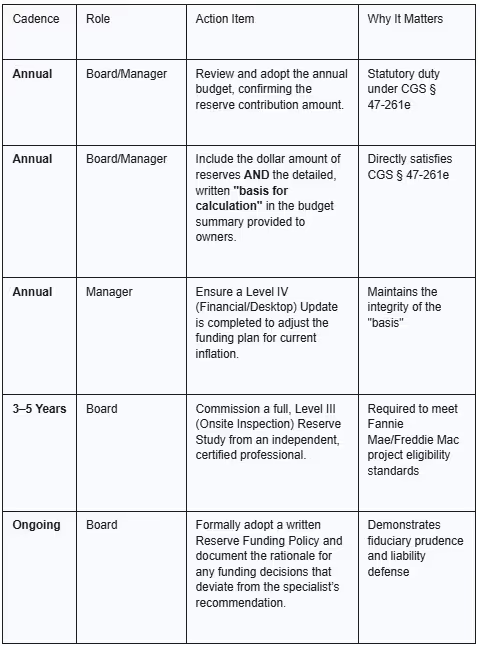

Your Board Compliance Checklist

For Connecticut HOA and COA boards and property managers, here are the essential action items to ensure compliance with CIOA and market standards:

Reimagine what a reserve study can do.

Stay informed. Stay prepared. And never get caught off-guard.

Asset Lifecyle Management

Save money and extend the life of assets by streamline the tracking of maintenence tasks and projects.

Integrated Financials

Drive better outcomes by seamlessly syncing third-party information.

Cash Flow Insights

Gain deeper clarity into your monthly cash position.

Future-Ready Financials

Design a roadmap for more predictable outcomes.

Today, over a half-million homes use the Living Reserve Study.

of Living Reserve Studies

Reserves Funding Capital Needs

Anticipated Capital Expenditures

Ready to get started?

Simplify operations, boost engagement, and manage smarter with SmartProperty.