A Guide to Hawaii Reserve Study Laws: Understanding Your HOA's Financial Future

Find state-specific reserve study requirements and funding laws — choose your state to see what is legally required for reserve studies, updates, and funding levels.

Hawaii’s unique legal landscape mandates one of the most rigorous and comprehensive reserve study frameworks in the United States, especially for condominium associations. These laws are designed to safeguard communities against deferred maintenance, sudden special assessments, and the cascading consequences of financial instability.

If you are a board member, property manager, or homeowner in the Aloha State, understanding these requirements is essential for maintaining compliance and protecting property values.

Executive Summary: The Big Picture

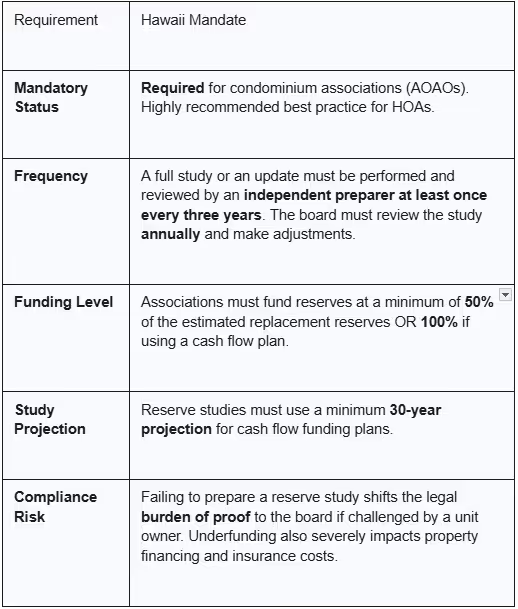

In Hawaii, the legal requirements for reserve studies depend on the type of association, but the standard for condominium boards is high.

Research Strategy

This briefing is based on an analysis of Hawaii’s primary governing legal source: the Hawaii Revised Statutes (HRS) Chapter 514B, known as the Condominium Property Act. All citations point directly to the relevant statutory language or authoritative commentary regarding reserve studies and funding.

Detailed Breakdown: Hawaii’s Reserve Study Requirements

Here is a deeper look into the specific legal mandates that govern community association reserves in Hawaii.

Is a Reserve Study Required or Recommended?

- Condominium Associations (AOAOs): Required. Hawaii law (HRS § 514B-148) explicitly mandates that condominium budgets include estimated replacement reserves based on a comprehensive reserve study.Planned Communities (HOAs) & Cooperatives: Recommended. While the statute does not mandate a reserve study for non-condominium associations, it is universally recognized as a "prudent business practice" and a fundamental element of the board’s fiduciary duty.

Applicability: Which Entities are Covered?

The mandatory requirements of HRS § 514B-148 apply exclusively to condominium associations (Associations of Apartment Owners or AOAOs).

There are specific requirements for component identification based on cost thresholds:

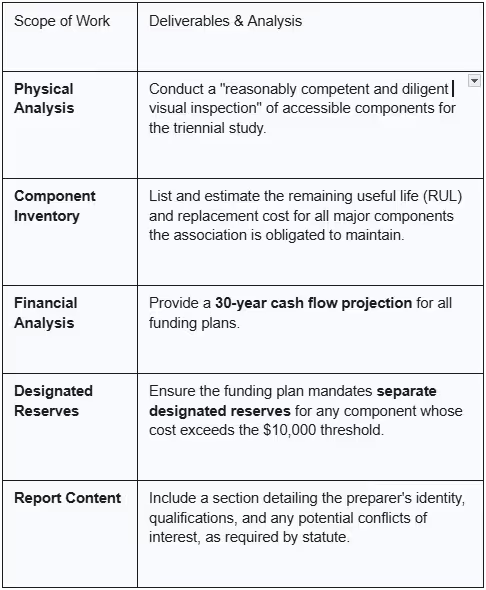

- $10,000 Threshold: The law requires separate, designated reserves for any component where the capital expenditure or major maintenance is estimated to exceed $10,000.

- Aggregation: Components with replacement costs not exceeding $10,000 may be aggregated into a single reserve fund.

Frequency/Cadence: How Often?

Hawaii employs a mandatory two-tiered cadence:

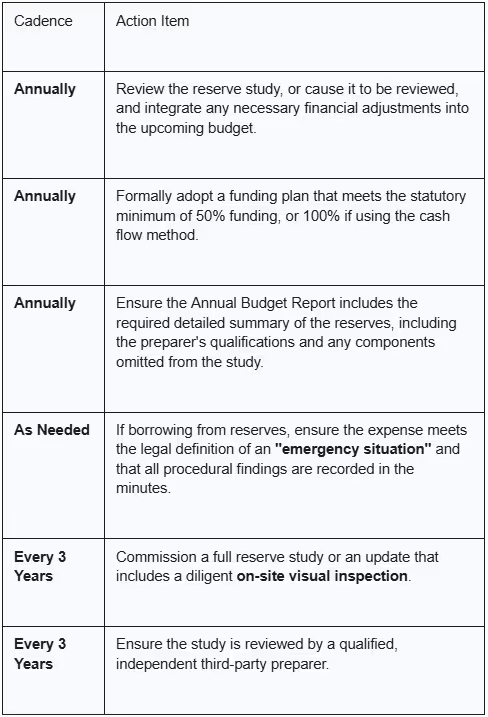

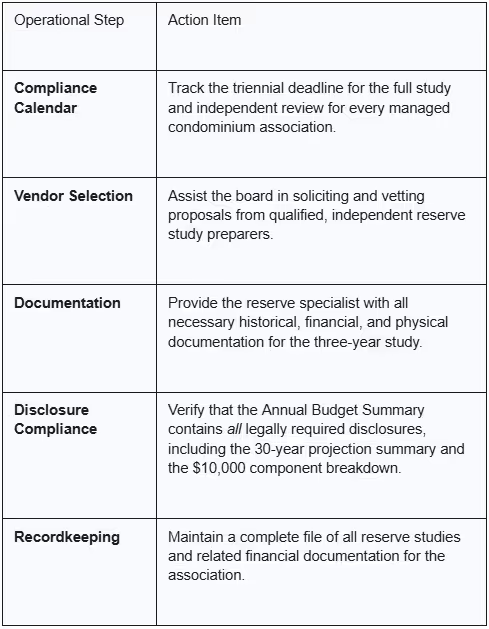

- Triennial Review (Site Visit Required): At least once every three years, the board must cause the reserve study to be reviewed or updated by an independent reserve study preparer. This triennial update must include a "reasonably competent and diligent visual inspection of the accessible areas of the major components".Annual Update (No Site Visit): The board must review the study, or cause it to be reviewed, annually. This internal review considers current financial figures and implements necessary adjustments to the funding plan.

- Method: Onsite/Visual Inspection Required?

Yes, the mandated triennial review must include a visual inspection. The study must identify major components the association is obligated to maintain, their probable remaining useful life, and the estimated cost for repair or replacement. The projection period for cash flow plans must be a minimum of 30 years.

Who May Perform It?

- Independence Required: While the association can prepare its own study, the law specifically states that the study, if not prepared by an independent preparer, shall be reviewed by an independent reserve study preparer at least every three years.

- Licensing/Certification: Hawaii law does not require a specific professional license or certification (such as a Reserve Specialist or Engineer) for the person performing or reviewing the study. However, the required disclosure compels the board to identify the preparer's qualifications and potential conflicts of interest Best practice dictates hiring a qualified professional with expertise in facilities, valuation, and financial modeling.

- Developer Exception: The initial reserve study included in a developer’s public report is not required to be prepared or reviewed by an independent third party.

Funding & Disclosures: Managing and Communicating the Money

Hawaii is unique in that it mandates specific minimum funding levels for condominium reserves:

- Minimum Funding: The association must assess and collect funds to meet a minimum of 50% of the estimated replacement reserves. This is the statutory floor.

- Cash Flow Funding: If the board adopts a "cash flow plan," it must fund at 100% of the estimated replacement reserves. The cash flow plan must be a minimum 30-year projection that is designed to fully meet future reserve needs without projecting special assessments or loans.

- Borrowing from Reserves: Funds are restricted for reserve purposes only. Reserves may only be used for other purposes in "emergency situations," which are narrowly defined (e.g., court order, threat to safety, unforeseen expenses, legal defense). Any non-emergency use may require approval by a majority of unit owners.

- Owner Disclosures: The annual budget provided to unit owners must include a summary with detailed disclosures on reserves, including the estimated reserve assessments required, a general explanation of how they were computed, and the identity/qualifications of the preparer.

Penalties & Risks: What Happens If You Don't Comply?

Non-compliance carries three primary risks for condominium associations:

- Civil Enforcement and Liability: A unit owner has standing to sue the board to compel compliance. If a board fails to prepare a study, it bears the legal burden of proving compliance in court. Board members who act in "good faith" are generally protected from personal liability if the reserve estimate is later proven incorrect.

- Lending Ineligibility: Underfunded reserves often result in a property becoming ineligible for mortgage financing from major lenders like Fannie Mae, Freddie Mac, FHA, and the VA. This severely limits the buyer pool, reducing the property's market value, often making units sellable only to cash buyers.

- Insurance Crisis: Low reserves signal poor maintenance to insurance carriers, leading to dramatically higher premiums (reported increases of 500% to 1,000%) or forcing the association into the unregulated excess/surplus market.

Forthcoming Changes & Practical Concerns

Legislative Horizon (2025 Session)

Hawaii's legislature has been highly active in response to recent insurance and financial crises, leading to significant reserve-related legislation.

- SB 1044 (Act 296, 2025) – Enacted: This pivotal law expands the state's capacity to address property insurance shortages and establishes the Condominium Loan Program. This program offers state-backed financing for essential repairs and deferred maintenance, directly addressing the systemic problem of underfunded reserves by providing a mechanism for associations to catch up on capital projects.

- SB 253 (2025 Session) – Status: Died in Chamber: This bill aimed to strengthen disclosure mandates by requiring that the annual budget summary include all required reserve information without relying on the reader to reference other documents. It also proposed removing the "good faith" liability defense for boards that omit the mandated detailed disclosure summary. While this specific bill did not pass, it signals a strong legislative focus on increasing board accountability and disclosure transparency.

Practical Concerns for Boards and Managers

- The "50% Funded" Trap: The difference between the legally allowed 50% minimum funding and 100% full funding is a frequent source of confusion. Boards must clearly communicate that while 50% is compliant, it exponentially increases the risk of needing a special assessment or loan for a catastrophic failure.

- Integration with Capital Projects: The establishment of the new state Condominium Loan Program through Act 296 (2025) means boards now have a state-sponsored option for remediation. Associations should proactively integrate this loan program into their financial risk modeling if they are severely underfunded or facing immediate major repairs.

Role-Based Checklists: Your Action Plan

HOA Board Checklist

Property Manager Checklist

Reserve Specialist Checklist

Reimagine what a reserve study can do.

Stay informed. Stay prepared. And never get caught off-guard.

Asset Lifecyle Management

Save money and extend the life of assets by streamline the tracking of maintenence tasks and projects.

Integrated Financials

Drive better outcomes by seamlessly syncing third-party information.

Cash Flow Insights

Gain deeper clarity into your monthly cash position.

Future-Ready Financials

Design a roadmap for more predictable outcomes.

Today, over a half-million homes use the Living Reserve Study.

of Living Reserve Studies

Reserves Funding Capital Needs

Anticipated Capital Expenditures

Ready to get started?

Simplify operations, boost engagement, and manage smarter with SmartProperty.