Maryland’s Mandatory Reserve Study & Funding Law (2025): The Complete Compliance Guide for HOAs and Condos

Find state-specific reserve study requirements and funding laws — choose your state to see what is legally required for reserve studies, updates, and funding levels.

Maryland is now one of the most rigorous states in the nation when it comes to long-term financial planning for community assets. This guide cuts through the legal jargon to give you the clear, actionable steps you need to ensure compliance, protect your community's investments, and mitigate fiduciary risk.

1. Is a Reserve Study Required in Maryland? (Binary + Nuance)

The short answer is Yes, it is mandatory.

Maryland law explicitly requires professional reserve studies and, crucially, mandates the budgeting and deposit of funds to implement the study’s findings. This compliance requirement covers nearly all standard community governance structures:

- Condominiums (COA): Required by the Maryland Condominium Act.

- Homeowners Associations (HOA): Required by the Maryland Homeowners Association Act.

- Cooperative Housing Corporations (Co-op): Required by the Maryland Cooperative Housing Corporation Act.

The HOA $10,000 Threshold

There is a specific, minor exemption for HOAs: a study is only required if the association is responsible for maintaining common areas and the total initial purchase and installation costs for all common area components amount to at least $10,000. Since this figure is based on

initial cost, almost every established HOA with a pool, clubhouse, or private street system will easily exceed this threshold and must comply.

2. Compliance Pillars: The 5-Year Cycle and the Funding Plan

Compliance is built around a continuous cycle of professional assessment and structured financial action.

The 5-Year Mandate (Cadence and Recurrence)

A full or updated professional reserve study must be completed at least once every 5 years .

- Initial Study: The initial deadline for most established associations has passed (varying by county/creation date, but generally by October 1, 2023) . Newly established HOAs must complete an independent study just before the turnover meeting.

- Updated Study: Once you have your initial study, you must maintain a recurring 5-year cycle for updates.

Methodology: The On-Site Inspection Requirement

While the law calls for an "updated reserve study," fulfilling the legal definition necessitates a physical, on-site visual inspection. A compliant study must assess and state the

estimated remaining useful life (EUL) of structural, mechanical, electrical, and plumbing components . Accurately assessing EUL requires a boots-on-the-ground visual assessment (often referred to as a Level II update in the industry).

The four mandatory elements of a compliant study are :

- Component Identification (Structural, MEP, etc.)

- Estimated Remaining Useful Life (EUL)

- Estimated Cost of repair or replacement

- Estimated Annual Reserve Amount needed

Annual Duty (Non-Study Review)

Boards must annually review the most recent reserve study or update to confirm funding adequacy in connection with the annual budget . This annual review does not require commissioning a new study every year—only the 5-year update is mandated .

3. The New Funding Mandate: HB 292 (Effective October 1, 2025)

The most significant change in Maryland law is the shift from disclosure to mandatory funding. House Bill 292 (Chapter 519, Laws of Maryland) introduces powerful new requirements, effective October 1, 2025.

Mandatory Funding Plan

The governing body must develop a formal Funding Plan in consultation with the reserve study author. This plan is the roadmap for achieving the recommended reserve levels.

The plan must specifically:

- Prioritize Safety and Structure: The plan must prioritize funding for components essential to occupant health, safety, and structural integrity (including roofing and structural systems), as well as essential functioning systems (plumbing, HVAC, electrical).

- Budget Alignment: Reserves provided in the annual budget shall be the funding amount recommended in the most recent study, following the adopted Funding Plan.

Mandatory Deposit Rule

To close any loophole, the law requires that the funds budgeted for reserves be deposited in the reserve account on or before the last day of each fiscal year. This ensures budgeted funds are physically segregated and protected.

Grace Period for Initial Funding Attainment

If the most recent study was your association's initial reserve study, the governing body has 5 fiscal years (extended from the previous 3-year requirement) following the year of completion to attain the recommended annual funding level.4

Financial Hardship Exception

A board may deviate from the funding requirements only by a two-thirds majority vote if they determine the association is experiencing a genuine financial hardship. This is a high bar, requiring detailed documentation and good-faith efforts to resolve the hardship.

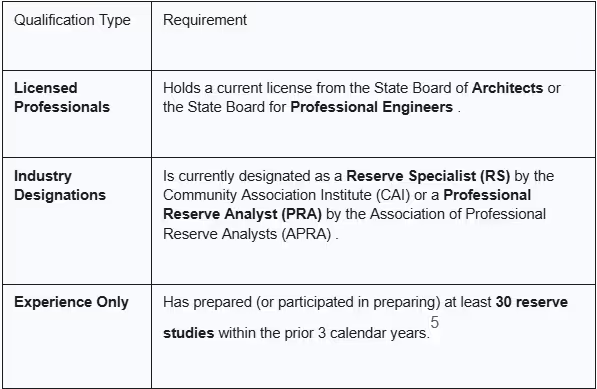

4. Qualifications for the Reserve Specialist

To guarantee professional objectivity, Maryland law mandates that the reserve study must be prepared by a person meeting specific professional qualifications :

Boards must verify that their chosen specialist meets at least one of these criteria.

5. Reserve Management, Disclosure, and Borrowing

Disclosure to Owners

The law mandates transparency. The board must submit a summary of the most recent reserve study to all owners concurrently with the distribution of the annual proposed budget. The complete reserve study must be made available for inspection and copying by any owner.

Rules for Borrowing from Reserves

The board is permitted to temporarily borrow from the reserve fund for capital projects or emergency repairs not listed in the Funding Plan. However, those borrowed funds must be repaid to the reserve fund within 5 years after their use.

6. Risks of Non-Compliance and Fiduciary Duty

Failure to meet these strict mandates carries significant risk for the association and its board members.

State Fines and Enforcement

The Maryland Attorney General's Office (Consumer Protection Division) is responsible for enforcing the Condominium Act . Non-compliance can lead to:

- Fines: Up to $10,000 .

- Discontinuance Orders: Orders compelling the association to comply .

Fiduciary Liability and the Funding Plan

Directors are generally protected by the Business Judgment Rule. However, the new Funding Plan (effective 2025) requires the explicit prioritization of structural and life-safety components. If a critical component fails due to underfunding, and the board failed to adopt or execute the prioritized plan, they could be vulnerable to claims of breach of fiduciary duty or gross negligence.

Lender and Marketability Risk

Inadequate reserve funding can render a condominium project ineligible for conventional mortgage financing through institutions like Fannie Mae and Freddie Mac. This means owners may struggle to sell or refinance their units, potentially freezing the market. Lenders now expect boards to align their funding plan with the recommendations of the professional reserve study.

7. The Future of Compliance: Key Takeaways

The most important takeaway for Maryland communities is the shift to proactive funding:

- 5-Year Cycle is Fixed: Maintain a disciplined cadence for updates with a qualified professional .

- Plan for the Funding Plan (2025): If you haven't yet, prepare to develop and formally adopt the mandatory Funding Plan by October 1, 2025, ensuring it prioritizes structural and life-safety elements.

- Deposit is Mandatory: The budgeted reserve amount must be transferred to the reserve account by the end of the fiscal year. Budgeting the funds is no longer enough.

- Review Annually: Board members must review their reserve study and progress toward the Funding Plan goal at every annual meeting.

Reimagine what a reserve study can do.

Stay informed. Stay prepared. And never get caught off-guard.

Asset Lifecyle Management

Save money and extend the life of assets by streamline the tracking of maintenence tasks and projects.

Integrated Financials

Drive better outcomes by seamlessly syncing third-party information.

Cash Flow Insights

Gain deeper clarity into your monthly cash position.

Future-Ready Financials

Design a roadmap for more predictable outcomes.

Today, over a half-million homes use the Living Reserve Study.

of Living Reserve Studies

Reserves Funding Capital Needs

Anticipated Capital Expenditures

Ready to get started?

Simplify operations, boost engagement, and manage smarter with SmartProperty.