New York Reserve Study Laws vs. a Board's Fiduciary Duty

Find state-specific reserve study requirements and funding laws — choose your state to see what is legally required for reserve studies, updates, and funding levels.

Unlike some states, New York state law does not explicitly mandate that community associations conduct reserve studies or maintain a minimum reserve fund balance. Most associations are formed under the New York Not-for-Profit Corporation Law (N-PCL) and their initial financial structure, including reserves (or lack thereof), is often outlined in the developer's Offering Plan. Some plans may even state, "There is no special advanced reserve fund".

This lack of a specific state mandate is often misinterpreted. It does not mean boards have no obligation regarding long-term financial planning. Instead, New York law relies heavily on the board's fundamental fiduciary duty, governed by corporate law.

What is a New York board's fiduciary duty? This is the highest standard of care, requiring directors to act for the benefit of the association (which they handle money and property for). It includes:

- Duty of Loyalty: Acting with "undivided loyalty" , putting the association's interests first, and avoiding self-dealing.

- Duty of Care: Acting "in good faith and with that degree of care which an ordinary prudent person... would use under similar circumstances". This requires making informed decisions.

- Duty to Act Within Authority: Operating strictly within the powers granted by governing documents and the law.

This fiduciary duty, particularly the Duty of Care, creates an implied obligation to plan for the association's long-term financial health, including predictable major repairs and replacements.

The New York Business Judgment Rule (BJR): A Shield for Boards

Recognizing that board members are often volunteers , New York courts use the Business Judgment Rule (BJR) to protect boards from liability for decisions made in good faith.11

Established in Levandusky v. One Fifth Ave. Apt. Corp. , the BJR states that courts will not second-guess a board's decision if the board can show the decision was :

- Made in good faith.

- Within the scope of its authority.

- In furtherance of corporate purposes.

However, this shield is not automatic. It must be earned.

Earning the BJR Shield: The "Informed Decision" Requirement

The BJR protects a business decision, implying a deliberate process. To gain BJR protection, a New York board must demonstrate its decision was informed. This requires:

- Investigation: Boards have an affirmative duty to investigate matters before acting. This applies to rule enforcement and especially financial planning.

- Deliberation, Not Procrastination: The BJR protects bad decisions made after deliberation, but it does not protect a failure to decide or simple inaction.

Crucially: A board that fails to investigate its long-term financial needs (e.g., by never commissioning a reserve study) or fails to deliberate on reserve funding may be deemed to have breached its Duty of Care procedurally. This failure can strip the board of BJR protection 8, allowing a court to review the merits of its (lack of) financial planning. Failing to fund reserves due to negligence or lack of diligence is likely not protected.

Special Assessments: The Symptom of Reserve Underfunding

The failure to adequately fund reserves for predictable, long-term replacements (like roofs or infrastructure ) inevitably leads to financial shortfalls. When these components fail, boards are often forced to levy large special assessments.

These assessments frequently trigger homeowner lawsuits. While the lawsuit targets the assessment, the underlying claim is typically breach of fiduciary duty, arguing the assessment is only necessary due to years of the board's negligence in failing to plan and fund reserves. To overcome the BJR, these lawsuits often allege the board acted in bad faith (e.g., self-dealing, discrimination).

Limits on Board Authority: The Pomerance Doctrine

A critical limitation on the BJR is that it only protects actions taken within the board's authority. If an action violates state law or the association's own governing documents (Declaration, Bylaws ), the BJR offers no protection.

The case Pomerance v. McGrath clarified this. Courts give no deference to a board's interpretation of its own authority. A court will first determine if the governing documents actually grant the power for the action (like a specific type of special assessment). Only after confirming authority will the court apply the BJR to the wisdom of the action. This allows homeowners to challenge board actions based on a straightforward breach of governing documents, bypassing the BJR.

The New Reality: Fannie Mae, Freddie Mac, and De Facto Reserve Mandates

Recent changes driven by mortgage giants Fannie Mae and Freddie Mac have drastically altered the landscape, creating a de facto minimum requirement for reserve funding in New York.

Following the Champlain Towers collapse, Fannie Mae and Freddie Mac implemented stricter requirements enforced through detailed lender questionnaires sent to associations. These questionnaires assess a building's "safety, soundness, integrity, and habitability" before a mortgage can be approved.

A key requirement is that at least 10% of the association's annual budgeted income must be allocated to reserves. This effectively acts as a mandate.

If an association fails to meet these requirements (including the 10% reserve rule, or having significant deferred maintenance), provides unacceptable answers, or fails to respond, the building can be listed as "non-warrantable".

- Impact: Lenders cannot issue conventional financing for units in non-warrantable buildings. This severely impacts owners' ability to sell or refinance and causes property values to drop.

This market reality overrides the BJR defense for failing to fund reserves. A decision not to fund reserves is no longer merely "unwise" ; it's arguably grossly negligent because it directly leads to the loss of financing eligibility and property value for all owners, a clear breach of the Duty of Care.

What is a Reserve Study? The Two Essential Parts

A professional reserve study is a long-term capital planning tool consisting of two parts: a physical analysis and a financial analysis.

Part 1: The Physical Analysis (What We Inspect)

A specialist conducts a visual, non-invasive inspection to assess the physical status of common property. This includes:

- Component Inventory: A list of major common area components the HOA must repair/replace.

- Condition Assessment: Evaluating the current condition of each component.

- Life & Valuation Estimates: Assigning Useful Life (UL), Remaining Useful Life (RUL), and estimating current Replacement Cost.

Part 2: The Financial Analysis (The Funding Plan)

This translates physical data into a financial roadmap.43 It includes:

- Fund Status: A snapshot of reserve health, often using "Percent Funded".

- Funding Plan: The core recommendation—a multi-year plan projecting income/expenses and suggesting a stable contribution amount.

How to Read a Reserve Study: 2 Key Metrics Explained

For a New York board, focus on these key metrics:

Metric 1: What is "Percent Funded" in a Reserve Study?

"Percent Funded" measures reserve strength. It is calculated as:

$$\text{Percent Funded} = \frac{\text{Reserve Fund Balance (actual cash on hand)}}{\text{Fully Funded Balance (computed deterioration)}}$$

"100% Funded" means the reserves match the computed deterioration of assets, not the total replacement cost of everything today. An industry rule of thumb suggests maintaining at least 70% funded to minimize the risk of special assessments.

Risk Profile :

- Strong (> 70% Funded): Low risk of special assessments.

- Fair (30% - 70% Funded): Moderate risk.

- Weak (< 30% Funded): High risk.

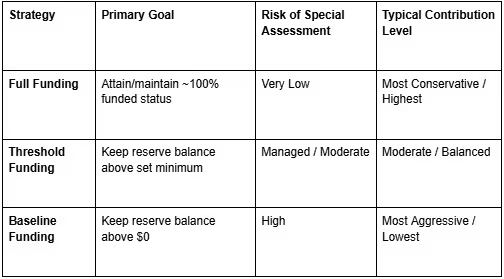

Metric 2: Choosing a Funding Goal (Full, Threshold, or Baseline)

The study presents funding goals, defining acceptable risk :

- Baseline Funding: Keeps balance just above $0. High risk, rarely recommended.

- Full Funding: Aims for ~100% funded. Low risk, most conservative.

- Threshold Funding: Keeps balance above a set minimum (e.g., 70%). Balanced, commonly recommended.

How to Implement a Reserve Study: A 5-Step Guide for New York Boards

For a New York board, implementing a study involves these steps :

Step 1: Understand the 3 Levels of a Reserve Study

Know what to ask for. National standards define three levels :

- Level I (Full Study): The essential first study. Involves full on-site inspection and inventory creation.

- Level II (Update with Site Visit): Periodic update (every 3-5 years recommended), specialist verifies inventory and re-assesses conditions on-site.

- Level III (Update, No Site Visit): Financial-only update for off-years.

Step 2: Pass a Board Resolution and Prepare Documents

Formally resolve to commission the study. Gather essential documents: Governing Documents, budgets, repair records.

Step 3: How to Hire a Credentialed Reserve Specialist

This is critical. Perform due diligence. Look for:

- Credentials: RS (Reserve Specialist) from CAI or PRA (Professional Reserve Analyst) from APRA.

- Standards: Adherence to CAI National Reserve Study Standards.

- Insurance: Proof of professional liability (Errors & Omissions) insurance.

Step 4: The Kick-Off Meeting and On-Site Inspection

Schedule a kickoff meeting and on-site inspection. Ensure someone knowledgeable accompanies the specialist. This is the "Physical Analysis".

Step 5: Review the Draft Report and Adopt the Funding Plan

Review the draft for factual errors. Formally vote to adopt the study and implement its funding plan into the next annual budget. This action documents the board's fulfillment of its fiduciary duty and helps meet lender requirements.

Conclusion: Why a Reserve Study is a Critical Action for Your New York Community

For a New York HOA, co-op, or condo board, commissioning and following a professional reserve study is no longer just a "best practice"—it is a necessary action to fulfill fiduciary duties, maintain property values, ensure financing eligibility, and protect board members from liability.

In New York, the reserve study is the tool that:

- Demonstrates fulfillment of the board's Duty of Care by ensuring decisions are "informed".

- Provides the basis for meeting the de facto 10% reserve allocation required by lenders.

- Protects homeowners from disruptive special assessments.

- Preserves property values and marketability by helping the building remain "warrantable".

- Strengthens the board's Business Judgment Rule defense.

A New York board that proactively uses a reserve study demonstrates responsible governance and takes the most critical step toward securing the community's financial and physical future.

Reimagine what a reserve study can do.

Stay informed. Stay prepared. And never get caught off-guard.

Asset Lifecyle Management

Save money and extend the life of assets by streamline the tracking of maintenence tasks and projects.

Integrated Financials

Drive better outcomes by seamlessly syncing third-party information.

Cash Flow Insights

Gain deeper clarity into your monthly cash position.

Future-Ready Financials

Design a roadmap for more predictable outcomes.

Today, over a half-million homes use the Living Reserve Study.

of Living Reserve Studies

Reserves Funding Capital Needs

Anticipated Capital Expenditures

Ready to get started?

Simplify operations, boost engagement, and manage smarter with SmartProperty.