Oregon Reserve Study Requirements: The Ultimate Guide for HOAs and Condos

Find state-specific reserve study requirements and funding laws — choose your state to see what is legally required for reserve studies, updates, and funding levels.

If you manage or serve on the board of a planned community (HOA) or condominium in Oregon, understanding reserve study compliance is non-negotiable.

Oregon law is unique—it requires a reserve analysis but offers flexibility on who performs it. However, the mortgage market imposes a much higher standard that most associations must meet to protect property values. This guide breaks down what is truly required, what lenders demand, and the major compliance risks you need to address today.

1. Is a Reserve Study Required in Oregon?

Yes, absolutely. It is a mandatory statutory requirement, not just a recommendation.

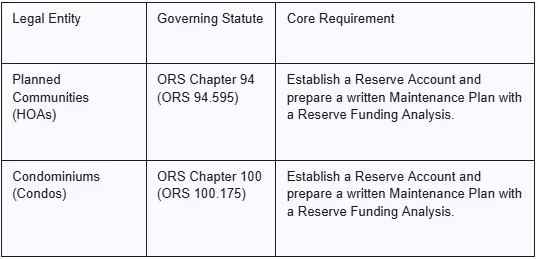

Oregon law uses the term "Maintenance Plan with Reserve Funding Analysis" rather than "reserve study," but the intent is the same: to mandate long-term financial planning for major component replacement.

Compliance Trigger for Older HOAs: If your planned community was recorded before October 23, 1999, the reserve requirements only apply if the board passes a resolution or a majority of owners submit a petition. If triggered, the initial study must be completed within one year .

Exemptions: Condominiums (governed by ORS 100), commercial/industrial subdivisions, timeshare plans, and certain new affordable housing developments are exempt from the ORS 94 Planned Community requirements.

2. Required Cadence and Scope of the Analysis

The process of reserve planning in Oregon is a two-part obligation: a mandatory annual review and a periodic physical assessment.

Mandatory Frequency: Annual Review

The law requires continuous financial oversight:

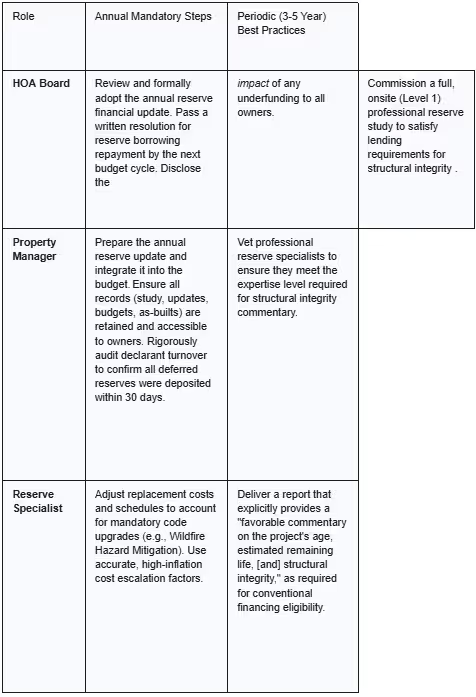

- The Maintenance Plan and Reserve Funding Analysis must be reviewed and updated annually.

- This updated analysis must be directly incorporated into the association’s annual operating budget.

This annual process aligns with what the industry calls a Level 3 (Financial) Update, ensuring your reserve contribution rates (inflation, interest returns, costs) are current, even if you skip a full onsite visit that year.

Recommended Cadence: Onsite Inspection

While the statute only mandates the annual financial update, industry best practice demands a full visual inspection to ensure the physical data is sound.

- Recommendation: Conduct a professional, onsite inspection (Level 1 or 2 study) every three to five years . This prevents budgeting based on obsolete data and reduces the risk of massive, unexpected special assessments.

Component Scope: The 1-to-30 Year Rule

Your reserve analysis must cover major common property components that will require major maintenance, repair, or replacement in more than one year and less than 30 years .

Examples include:

- Roofs

- Siding

- Paving

- Exterior painting (if applicable)

3. Who May Perform the Reserve Study? (The Lender Mandate)

This is where Oregon compliance creates a major catch-22 for boards.

Statutory Flexibility

Oregon law is highly flexible on who prepares the analysis. ORS Chapters 94 and 100 do not require the study to be performed by a licensed, certified, or third-party professional . Boards are technically allowed to conduct the reserve funding analysis internally.1

The Real-World Requirement: Fannie Mae and Freddie Mac

Relying on an internal, non-professional analysis risks rendering your units virtually unmarketable. Secondary mortgage market lenders (Fannie Mae and Freddie Mac) set standards that dictate whether owners can get conventional mortgages. These standards create a de facto requirement for a professional, third-party study.

Lenders require the reserve study to:

- Comment Favorably on Structural Integrity: The study must explicitly address the project's structural integrity and the estimated remaining life of major components. Only a certified professional (like a Reserve Specialist, Engineer, or Architect) can reliably provide this commentary.8

- Validate Funding: The analysis must "validate that the project has appropriately allocated the recommended reserve funds".8

The Bottom Line: To ensure owners can sell or refinance units, your association must adhere to the high standards of the lending market, effectively making a professional, independent reserve study a necessity.

4. Key Financial and Funding Regulations

Governing the Use of Reserve Funds

Reserves are protected, but the board has limited borrowing flexibility.

- Permitted Borrowing: The board may temporarily borrow from reserves only for two reasons: (1) to meet high seasonal demands on the operating fund, or (2) to cover unexpected increases in expenses.

- Mandatory Repayment: If funds are borrowed, the board must adopt a written resolution detailing the repayment plan. Repayment must be completed by no later than the adoption of the budget for the following year.

Risk Alert: Failure to adopt this written repayment resolution and meet the strict repayment deadline is a clear breach of statutory duty and a significant liability risk for the board.

Declarant Turnover and Deferred Reserves

For new communities, the developer (Declarant) can defer reserve assessments until a lot is conveyed, but this deferment cannot extend past the official turnover meeting.11

- Financial Due Diligence: The Declarant must deposit the balance due for all deferred reserve assessments within 30 days after the turnover deadline.11

- Transparency: The association’s books and records must clearly reflect the exact amount the declarant owes for these deferred assessments.11 Boards and managers must audit this immediately at turnover.

5. Transparency, Disclosure, and Board Risk

Oregon law mandates strict transparency, forcing boards to confront owners with the consequences of underfunding.

Required Owner Disclosures

The annual budget must not only disclose the reserve contribution levels but also explicitly outline the impact of not adequately funding reserves.

- Example: A compliant disclosure might state: "Insufficient funding at the recommended level of 80% increases the likelihood of a $X,000 per-unit special assessment within the next five years to cover the roofing project."

Recordkeeping Mandates

The association must maintain and make available to owners for inspection the following documents.

- The Reserve Study and Maintenance Plan (including all annual updates and underlying data).

- The Operating Budget and the Reserve Budget.

- Copies of "as-built" architectural, structural, and engineering documents, if available.

Board Liability and Non-Compliance

While ORS does not specify a fine for failing to reach a specific funding percentage, boards face liability exposure for procedural non-compliance .

- High-Risk Actions: Failure to establish the reserve account , failure to create the written maintenance plan , or failure to adopt and execute the written repayment resolution for borrowed funds are all clear violations of statutory duty.

6. Forthcoming Changes and Interacting Laws

While Oregon is not currently implementing a comprehensive, state-mandated structural inspection law, other code and regulatory forces are influencing reserve costs.

No Mandatory Structural Inspection Law (Yet)

As of the current date, Oregon does not require mandatory periodic structural inspections for condos or HOAs, unlike some coastal states.

However, the Lender Mandate Remains Key: As noted in Section 3, the financial market's demand for a professional structural commentary in the reserve study acts as the de facto structural due diligence check.

The Impact of Modern Building Codes (ORSC)

Reserve specialists and boards must account for changing building codes, as they dramatically increase future replacement costs.14

- Wildfire Hazard Mitigation: Recent changes to the Oregon Residential Specialty Code (ORSC), including amendments related to Wildfire Hazard Mitigation (R327), are mandatory. When a component like a roof or siding is scheduled for replacement, it must be upgraded to meet current fire-resistant code standards.

- Actionable Tip: Reserve specialists must integrate these mandated code upgrades into their replacement cost calculations to prevent future underfunding.

Action Plan Checklist for Oregon Professionals and Boards

Reimagine what a reserve study can do.

Stay informed. Stay prepared. And never get caught off-guard.

Asset Lifecyle Management

Save money and extend the life of assets by streamline the tracking of maintenence tasks and projects.

Integrated Financials

Drive better outcomes by seamlessly syncing third-party information.

Cash Flow Insights

Gain deeper clarity into your monthly cash position.

Future-Ready Financials

Design a roadmap for more predictable outcomes.

Today, over a half-million homes use the Living Reserve Study.

of Living Reserve Studies

Reserves Funding Capital Needs

Anticipated Capital Expenditures

Ready to get started?

Simplify operations, boost engagement, and manage smarter with SmartProperty.