A Guide to Vermont Reserve Study Laws: Understanding Your HOA's Financial Future

Find state-specific reserve study requirements and funding laws — choose your state to see what is legally required for reserve studies, updates, and funding levels.

The legal situation in Vermont is clear: Vermont state law does not explicitly require established condo associations or HOAs to conduct formal reserve studies or maintain a minimum reserve fund balance throughout the life of the association.

- Association Powers: The Vermont Common Interest Ownership Act (VCIOA), specifically 27A V.S.A. § 3-102(a)(2), grants the association the legal power to "adopt and amend budgets for revenues, expenditures, and reserves" and collect assessments to fund them. However, this is an authorization ("may"), not a command ("shall").

- Developer Disclosure: The law (27A V.S.A. § 4-103(a)(5)) does require the initial developer's Public Offering Statement for a new community to include the amount budgeted for reserves or state that there is no amount included. After this initial disclosure, the statute doesn't mandate ongoing studies or funding levels by the homeowner-controlled association.

This absence of an ongoing state mandate is often misinterpreted as a "pass" on reserve planning. This is a critical—and potentially costly—misunderstanding. In Vermont, the lack of specific state rules elevates the importance of the board's general fiduciary duty.

What is a Vermont HOA board's fiduciary duty? This legal standard requires board members to act in "good faith," with loyalty, and with the care an "ordinarily prudent person" would exercise in similar circumstances. This includes making informed decisions ("reasonable inquiry") and exercising prudent financial management regarding the association's assets.

This creates a paradox: the lack of a specific law requiring a study makes having one even more important in Vermont. If a major component fails (like a roof, siding, or boiler) requiring a large special assessment because the board didn't plan, homeowners can sue the board for negligence and breach of fiduciary duty. Without a state law checklist, the board's only defense is proving its actions met the "ordinary prudence" standard.

A professional reserve study provides that proof for a Vermont board. It demonstrates the board fulfilled its Duty of Care by making informed decisions based on expert analysis, not guesswork.

What are the Benefits of a Reserve Study? The 4 Key Pillars for Vermont Communities

Even without a state mandate, proactively commissioning a reserve study provides crucial benefits for Vermont communities.

Benefit 1: Avoid Special Assessments and Ensure Financial Stability

A reserve study shifts financial planning from reactive (special assessments) to proactive. It helps avoid sudden, large bills for homeowners when predictable failures occur. The "special assessment" model is also unfair—long-term owners might enjoy years of artificially low dues, only for new owners to face a massive bill for deterioration that occurred before they arrived. A reserve study creates an equitable plan where owners contribute fairly over time.

Benefit 2: Protect and Increase HOA Property Values in Vermont

A reserve study acts as a "maintenance planning tool". By ensuring funds are available, the association can perform repairs and replacements on schedule, preventing "deferred maintenance" that leads to disrepair and lowers property values., Well-maintained common areas directly correlate with higher property values in Vermont. Poor reserves can significantly decrease property values.

Benefit 3: Meet Lender Requirements (Fannie Mae & FHA)

A home's value is tied to a buyer's ability to get a mortgage. Lenders like Fannie Mae and FHA have requirements regarding an association's financial health. Fannie Mae requires lenders to review reserve adequacy, and FHA often requires 10% of income be allocated to reserves. Since Vermont law requires disclosing reserve amounts via the Resale Certificate (27A V.S.A. 4-109), lenders will see this information. An association showing low or non-existent reserves can be placed on a lender's "ineligible" list, hurting marketability and property values.

Benefit 4: Provide an Objective Roadmap for Future Vermont Boards

A reserve study is an essential governance tool. Board members and managers change, but the study provides continuity and explains the reasoning behind financial decisions. It's an "unbiased and objective" roadmap that depoliticizes budget discussions.5 The board isn't the "bad guy" for funding reserves; it's fulfilling its fiduciary duty based on an expert plan.

What is a Reserve Study? The Two Essential Parts

A professional reserve study is a long-term capital planning tool consisting of two parts: a physical analysis and a financial analysis.

Part 1: The Physical Analysis (What We Inspect)

A specialist conducts a visual, non-invasive inspection to assess the physical status of common property. This includes:

- Component Inventory: A list of major common area components the HOA must repair/replace. Components typically meet a four-part test: association responsibility, limited useful life, predictable remaining life, and material cost.

- Condition Assessment: Evaluating the current condition of each component.

- Life & Valuation Estimates: Assigning Useful Life (UL), Remaining Useful Life (RUL), and estimating current Replacement Cost, including all related costs.

Part 2: The Financial Analysis (The Funding Plan)

This translates physical data into a financial roadmap. It includes:

- Fund Status: A snapshot of reserve health, often using "Percent Funded".

- Funding Plan: The core recommendation—a multi-year plan (typically 20-30 years) projecting income/expenses and suggesting a stable contribution amount.

How to Read a Reserve Study: 2 Key Metrics Explained

For a Vermont board, focus on these key metrics:

Metric 1: What is "Percent Funded" in a Reserve Study?

"Percent Funded" measures reserve strength. It is calculated as:

$$\text{Percent Funded} = \frac{\text{Reserve Fund Balance (actual cash on hand)}}{\text{Fully Funded Balance (computed deterioration)}}$$

This formula compares your actual cash reserves to the calculated value of the wear-and-tear (deterioration) on your assets. "100% Funded" means the reserves match the computed deterioration, not the total replacement cost of everything today. An industry rule of thumb suggests maintaining at least 70% funded to minimize the risk of special assessments.

Risk Profile:

- Strong (> 70% Funded): Low risk of special assessments.

- Fair (30% - 70% Funded): Moderate risk.

- Weak (< 30% Funded): High risk.

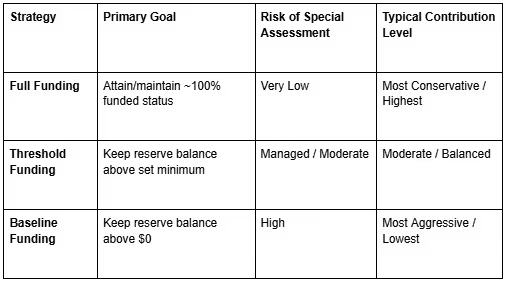

Metric 2: Choosing a Funding Goal (Full, Threshold, or Baseline)

The study presents funding goals, defining acceptable risk levels:

- Baseline Funding: Keeps balance just above $0. High risk, rarely recommended.

- Full Funding: Aims for ~100% funded. Low risk, most conservative.

- Threshold Funding: Keeps balance above a set minimum (e.g., 70%). Balanced, commonly recommended.

How to Implement a Reserve Study: A 5-Step Guide for Vermont Boards

For a Vermont board, implementing a study involves these steps :

Step 1: Understand the 3 Levels of a Reserve Study

Know what to ask for. National standards define three levels:

- Level I (Full Study): The essential first study. Involves full on-site inspection and inventory creation.

- Level II (Update with Site Visit): Periodic update (every 3-5 years recommended), specialist verifies inventory and re-assesses conditions on-site.

- Level III (Update, No Site Visit): Financial-only update for off-years.

Step 2: Pass a Board Resolution and Prepare Documents

Formally resolve to commission the study. Gather essential documents: Governing Documents (defining maintenance responsibilities), budgets, and repair records.

Step 3: How to Hire a Credentialed Reserve Specialist

This is critical. Perform due diligence. Look for:

- Credentials: RS (Reserve Specialist) from CAI or PRA (Professional Reserve Analyst) from APRA. These require experience and adherence to standards.

- Standards: Adherence to CAI National Reserve Study Standards.

- Insurance: Proof of professional liability (Errors & Omissions) insurance.

Step 4: The Kick-Off Meeting and On-Site Inspection

Schedule a kickoff meeting and the on-site inspection. Ensure someone knowledgeable accompanies the specialist. This is the "Physical Analysis".

Step 5: Review the Draft Report and Adopt the Funding Plan

Review the draft for factual errors. Formally vote to adopt the study and, most importantly, implement its funding plan into the next annual budget. This action documents the board's fulfillment of its fiduciary duty.

Vermont's Enforcement: The Mandatory Resale Certificate (27A V.S.A. 4-109)

While Vermont doesn't mandate reserve funding, it does mandate financial transparency at the point of sale via the Resale Certificate required by 27A V.S.A. 4-109. This certificate must be provided by the association to the seller (upon request) for delivery to the buyer.

Legally Required Disclosures on the Vermont Resale Certificate:

27A V.S.A. 4-109 specifically requires the certificate to disclose key financial data, similar to Missouri's law:

- "Any capital expenditures anticipated by the association for the current and two next succeeding fiscal years." (Shows the board's 3-year plan, or lack thereof).

- "The amount of any reserves for capital expenditures." (A specific dollar amount reflecting financial health).

- "Any portions of those reserves designated by the association for any specified projects." (Shows if reserves are allocated or just a general fund).

How the Resale Certificate Creates Accountability:

This legally required document is powerful for both buyers and current homeowners.

- Market Pressure: A certificate showing low reserves signals high risk to buyers and lenders, potentially lowering property values or hindering sales. This pressures boards to maintain healthier reserves.

- Legal Liability for Errors: Just as in New Mexico, if the association makes an error and fails to disclose a fee (like an approved special assessment) on the certificate, the buyer is generally not liable for that undisclosed amount. The association could be legally prevented (estopped) from collecting it, creating a financial loss due to negligence.

Conclusion: Why a Reserve Study is a Critical Investment for Your Vermont Community

For a Vermont HOA or condo board, commissioning a reserve study is the most effective way to fulfill your fundamental fiduciary duty, protect the community's assets, and ensure compliance with state disclosure laws.

In Vermont, the reserve study is the mechanism that:

- Fulfills the board's "prudent person" Duty of Care.

- Protects homeowners from unfair and potentially challengeable special assessments.

- Preserves and enhances property values.

- Ensures transparency and provides the data needed for the mandatory Resale Certificate disclosures (27A V.S.A. 4-109).

- Provides objective justification for budget decisions.

A Vermont board that proactively commissions a reserve study demonstrates responsible management, meets its legal obligations effectively, and secures the community's financial future.

Reimagine what a reserve study can do.

Stay informed. Stay prepared. And never get caught off-guard.

Asset Lifecyle Management

Save money and extend the life of assets by streamline the tracking of maintenence tasks and projects.

Integrated Financials

Drive better outcomes by seamlessly syncing third-party information.

Cash Flow Insights

Gain deeper clarity into your monthly cash position.

Future-Ready Financials

Design a roadmap for more predictable outcomes.

Today, over a half-million homes use the Living Reserve Study.

of Living Reserve Studies

Reserves Funding Capital Needs

Anticipated Capital Expenditures

Ready to get started?

Simplify operations, boost engagement, and manage smarter with SmartProperty.