Washington State Reserve Study Requirements: Your HOA/Condo Compliance Roadmap

Find state-specific reserve study requirements and funding laws — choose your state to see what is legally required for reserve studies, updates, and funding levels.

For HOA and Condominium boards in Washington State, a reserve study is not a suggestion—it is a clear legal mandate. Understanding the law is the critical first step to securing your community’s financial health, preventing massive special assessments, and protecting property marketability.

1. Is a Reserve Study Legally Required in Washington? (Binary + Nuance)

The Answer is Yes. Washington State requires that most residential common interest communities (CICs)—including condominiums and homeowners' associations—prepare and maintain a reserve study.1

- Condos (RCW 64.34) and HOAs (RCW 64.38): Associations with "significant assets" are required to prepare and update a study unless doing so would impose an "unreasonable hardship".1 Because these terms are not clearly defined in the statute, relying on them for exemption is a significant risk.1

- Small Association Waiver: A limited exception exists for condominiums with ten or fewer units. These associations can waive the study requirement, but only if two-thirds of the unit owners agree, and this vote must be renewed every three years.1 Even if waived, the lack of a study

must be disclosed on all resale certificates.1 - New or Transitioning Communities (WUCIOA/RCW 64.90): Newer communities, or those governed by the Washington Uniform Common Interest Ownership Act (WUCIOA), are strictly mandated to maintain a study unless they are restricted to nonresidential use, have nominal reserve costs, or if the study cost exceeds 10% of the annual budget.1

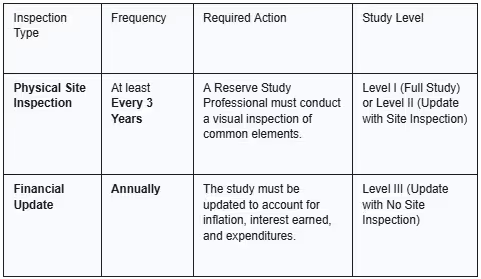

2. The Compliance Cadence: How Often Must You Inspect?

Washington law demands a rigorous, two-part schedule that ensures both the financial projections and the physical data remain accurate.2

This structure ensures your financial planning is constantly monitored, but the physical assumptions (lifespan and cost) are rigorously re-verified on a 36-month cycle.

3. Who Can Perform the Reserve Study? (Independence is Key)

The qualifications for the preparer are defined by statute, but market demands often set a higher standard for financial safety.

- Definition of a Professional: A "Reserve Study Professional" is an independent person suitably qualified by knowledge, skill, and experience.State licensing is not legally required.

- The Independence Rule: The initial study and the triennial site inspections must be performed by a professional. If the study is prepared internally, it must be reviewed by an independent party at least every three years.

- Property Manager Status: A managing agent who holds industry reserve study designations is not considered a conflict of interest for the purposes of conducting this triennial independent review.

4. Required Content: The 1% Rule and Funding Plans

Washington law is highly prescriptive about what must be included in your report (RCW 64.38.070).

A. Component Inclusion (The 1% Rule)

The study must include a list of all reserve components—from roofing and paving to decks and siding—whose cost for major maintenance or replacement would exceed one percent (1%) of the association's annual budget (excluding the reserve contribution itself). If a component that meets this threshold is excluded, the professional must provide commentary explaining the rationale.

B. Mandatory Funding Plan Presentation

To equip the board with planning options, the report must present three distinct funding strategies :

- Full Funding Plan: The contribution rate required to achieve 100% funding status by the end of the 30-year study period.

- Baseline Funding Plan: The contribution rate needed to ensure the reserve balance never drops below zero throughout the 30-year period (a high-risk option).

- Recommended Contribution Rate: The specific rate recommended by the Reserve Study Professional.

C. Required Disclosures to Owners

Every reserve study must include a specific statutory disclosure :

"This reserve study should be reviewed carefully. It may not include all common and limited common element components that will require major maintenance, repair, or replacement in future years... The failure to include a component in a reserve study, or to provide contributions to a reserve account for a component, may, under some circumstances, require you to pay on demand as a special assessment your share of common expenses...".

5. Funding and Borrowing Restrictions

While Washington law encourages associations to establish a reserve account , it does

not mandate a specific funding percentage (e.g., 70% funded).4 However, the law is strict on how reserve funds can be used (RCW 64.90.540).

- Borrowing for Operational/Non-Reserve Costs: If the board withdraws funds for unforeseen or unbudgeted operational costs (unrelated to replacement), the withdrawal must be recorded in the minutes, owners must be notified, and the board must adopt a mandatory repayment schedule not to exceed 24 months.

- Borrowing for Unbudgeted Replacement: Funds can be withdrawn to pay for unexpected replacement costs of reserve components not included in the current study without the 24-month repayment restriction.

6. Forthcoming Changes: The Critical 2028 Deadline

The single most important legislative change on the horizon is the expiration of key exemptions for Homeowners' Associations.

- The Sunset Date: Exemptions under RCW 64.38 (which include the small association rule and the 5% cost-to-budget exemption) will expire on January 1, 2028.

- The Impact: After this date, nearly all residential HOAs will be governed by the stricter, standardized requirements of WUCIOA (RCW 64.90.545).1 Boards currently relying on older exemptions should immediately begin the mandatory triennial inspection cadence to ensure compliance.

7. Practical Concerns: Why Compliance Protects Your Property Value

While the state’s statutory civil penalty for willful non-compliance is relatively small (up to $1,000 to an owner) , the true danger lies in property marketability.

- Lender Compliance is Key: Fannie Mae and Freddie Mac require associations to maintain project eligibility for conventional financing. To do this, they demand a current reserve study or update completed within three years of a loan approval date.

- The De Facto 10% Rule: Lenders often require the association to budget a minimum of 10% of annual assessments for reserves.11 If you wish to budget a lower amount, the

only way to secure an exemption and maintain project eligibility is with a current reserve study prepared by an independent third party that justifies the lower rate.

In short: To protect your community's marketability and financial stability, you must adhere to the higher standard of a triennial independent third-party site inspection and ensure your funding policy is supported by the professional’s recommendations.

Reimagine what a reserve study can do.

Stay informed. Stay prepared. And never get caught off-guard.

Asset Lifecyle Management

Save money and extend the life of assets by streamline the tracking of maintenence tasks and projects.

Integrated Financials

Drive better outcomes by seamlessly syncing third-party information.

Cash Flow Insights

Gain deeper clarity into your monthly cash position.

Future-Ready Financials

Design a roadmap for more predictable outcomes.

Today, over a half-million homes use the Living Reserve Study.

of Living Reserve Studies

Reserves Funding Capital Needs

Anticipated Capital Expenditures

Ready to get started?

Simplify operations, boost engagement, and manage smarter with SmartProperty.